Picture this: You are lying in bed on a warm summer night in Lahore. Suddenly, the sky opens up. A massive 2026 monsoon storm rolls in, bringing heavy winds and pounding hail that echoes through your entire house. You wake up the next morning, step outside, and your heart sinks. There are missing shingles scattered across your lawn, and a suspicious brown water stain is starting to bloom on your living room ceiling.

Panic sets in. You know roof repairs are incredibly expensive, but you also pay your home coverage premiums every single month for a reason. This leads you to the ultimate question: how does an insurance claim on a roof work?

If you have never filed a claim before, the process can feel like a complicated maze of technical jargon, adjusters, and paperwork. But understanding the roof repair claim process is absolutely crucial. According to recent industry reports, roof-related issues account for nearly 40% of homeowner claims. Knowing exactly what to do saves you time, keeps more money in your pocket, and eliminates the massive stress of the unknown.

| Step | Description |

|---|---|

| Assess Damage | Inspect roof immediately after event; document with photos/videos of issues like missing shingles or leaks. Make temporary fixes (e.g., tarps) to prevent worsening, keeping receipts. |

| Review Policy | Check coverage type (ACV vs. RCV), deductibles, and exclusions (e.g., wear/tear not covered). Act within policy timelines, often 48 hours. |

| Get Contractor Inspection | Hire reputable roofer for professional report; they can identify hidden damage. |

| File Claim | Call insurer to report; provide details, evidence, and claim number. Contractor may file or use Assignment of Benefits. |

| Adjuster Visit | Insurer sends inspector; have contractor present to explain damage. Adjuster approves/denies and estimates cost. |

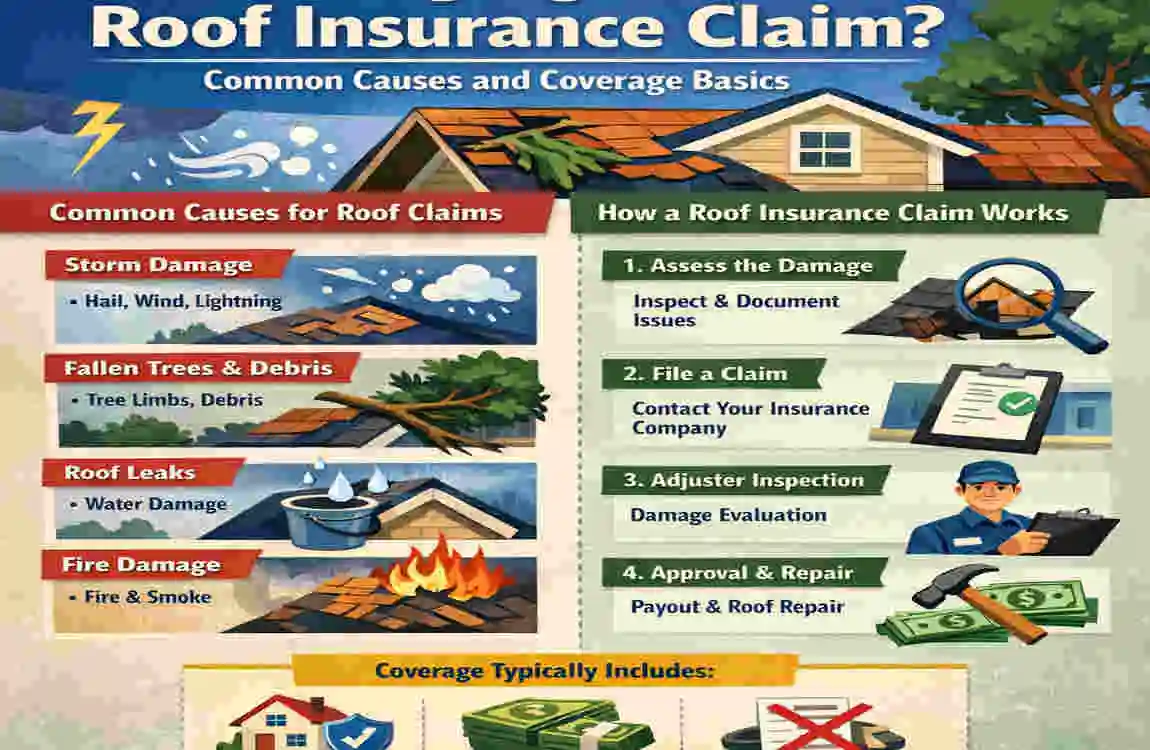

What Triggers a Roof Insurance Claim? Common Causes and Coverage Basics

Before you pick up the phone to file a claim, you need to know if your specific problem is actually covered. Homeowners insurance is designed to protect you from sudden, unexpected disasters. It is not a maintenance plan for an old, worn-out house.

Generally speaking, a standard policy covers damage caused by extreme weather and unavoidable accidents. However, it will strictly exclude damage caused by normal wear and tear, age, or poor maintenance.

Common Triggers for a Roof Damage Claim

Here are the most common reasons homeowners successfully file a roof claim:

- Storms and Natural Disasters: This is the big one. The heavy 2026 monsoon impacts in regions like Punjab have caused widespread damage from wind, hail, and rainfall. If a sudden storm rips the materials off your house, you are usually covered.

- Fallen Trees and debris: If a healthy tree in your yard snaps during a windstorm and crashes through your attic, your policy will typically cover the removal of the tree and the structural repairs.

- Sudden Accidental Fires: Whether it is a kitchen fire that spreads upward or a lightning strike, fire damage is covered under standard coverage.

- Manufacturing Defects: Occasionally, the materials used to build your house fail prematurely due to factory errors. Depending on your policy, sudden leaks caused by these defects might be covered.

Understanding Your Coverage Types: ACV vs. RCV

When you ask, “Does insurance cover roof replacement?”, the answer depends entirely on the type of coverage you bought. There are two main ways insurance companies calculate your payout. Let us break down these complex ideas into simple terms.

Coverage Type: What It Means in Simple Terms: Pros: Cons:

Actual Cash Value (ACV) Pays you what your roof is worth today, factoring in its age and condition. Monthly premiums are much cheaper. You get a smaller payout and must pay the difference for a new roof out of pocket.

Replacement Cost Value (RCV) pays the exact current market price to build a brand-new roof of similar quality. Provides maximum financial protection in the event of a disaster. Monthly premiums are higher, and you must actually complete the repairs to get full funds.

A Note for Our Local Readers

If you live in Pakistan, navigating local building codes and regional insurers adds another layer to the process. Companies like EFU General Insurance or Jubilee General Insurance have specific protocols for weather-related damage. When filing a homeowner’s roof claim here, ensure your repairs comply with the latest Lahore building safety codes, especially regarding heat-resistant materials and proper drainage during heavy rain.

Are you wondering if your specific situation qualifies for a full replacement? Keep reading, because we are going to break down the exact steps you need to take right now.

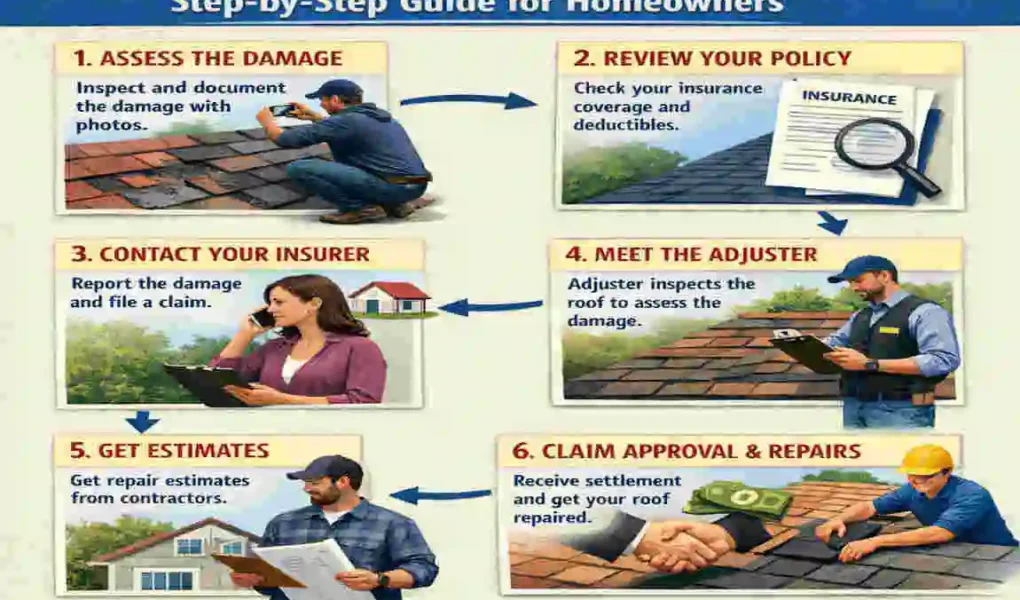

Step-by-Step: How Does an Insurance Claim on a Roof Work?

When disaster strikes, your adrenaline is pumping. It is easy to make a mistake that could jeopardize your payout. To ensure you get the money you deserve, you need to follow a strict blueprint.

Here is exactly how you navigate filing a roof claim step by step.

Assess the Damage Immediately

The moment it is safe to go outside, you need to investigate. However, safety comes first. Never climb onto a wet, slippery, or structurally compromised roof. Leave the climbing to the professionals.

Instead, walk around your property and document everything from the ground. Use your smartphone to take clear, well-lit photos and videos of the damage. If a tree fell, film it from multiple angles. If you have interior water stains, take pictures of your ceiling and any damaged furniture below it.

Look for these signs of claim-worthy damage:

- Shingles or tiles lying in your yard.

- Visible cracks, dents, or bald spots on your roofing materials.

- Dented gutters or damaged window screens (hail usually hits these, too).

- Water is pooling in your attic or dripping down your walls.

This early documentation is the foundation of your entire claim.

Review Your Policy and Notify Your Insurer

Once you have your photos, sit down and pull up your policy details online or via your provider’s mobile app. You want to check three things: your deductible (the amount you pay before the insurance kicks in), your coverage limits, and any specific exclusions.

You need to file your claim promptly, ideally within 24 to 72 hours of the event. Delays give the provider room to argue that the damage worsened because you neglected it.

Hire a Professional Inspector or Contractor

Do not wait for the insurance company to send their person before you get your own expert opinion. Why? Because DIY inspections weaken claims. You might miss hidden structural damage that a trained eye would catch immediately.

Reach out to 2 or 3 reputable, local contractors for an independent assessment. If you are in our area, we always recommend using highly rated Lahore roofers who understand local weather patterns. A good contractor will climb the structure, mark the damage with chalk, take professional photos, and prepare a detailed estimate of the cost to repair it. You will use this estimate as leverage later.

The Adjuster’s Inspection and Estimate

After you file, the insurance company will assign an adjuster to your case. This person works for the insurance company and verifies the damage and estimates repair costs.

When they visit your house, they will measure the damaged areas and take their own photos. In 2026, we are seeing a massive trend of adjusters using high-tech drones to inspect steep or dangerous properties without ever having to pull out a ladder.

How to handle the adjuster: Always have your personal contractor present during the adjuster’s visit. If the adjuster offers a lowball estimate that barely covers the materials, your contractor can step in, point out the hidden damage, and present the independent quote you gathered in Step 3. Do not be afraid to negotiate.

Approve the Payout and Repairs

Once everyone agrees on the scope of the damage, the company will approve your claim. On average, this timeline takes about 30 to 60 days from the date of the storm to the moment you get a check.

Usually, the insurer sends you a first check for the roof‘s Actual Cash Value. You will use this money to start the repairs.

What happens if your contractor tears off the old materials and finds rotten wood underneath that no one saw? Do not panic. Your contractor will file a supplemental claim with the insurer to cover these hidden, unforeseen costs.

Complete Repairs and Close the Claim

With the first check in hand, it is time to get to work. Choose a reputable, licensed contractor to do the job. Avoid door-to-door salespeople who promise to waive your deductible in exchange for a cash deal—this is often considered insurance fraud and can land you in serious legal trouble.

Once the repairs are finished, your contractor will send a final invoice to the insurance company. If you have a Replacement Cost Value policy, the insurer will then send you a second check to cover the remaining balance. After the final payment clears, your claim is officially closed, and you have a beautiful, safe home once again!

Does Homeowners Insurance Always Cover Roof Claims? Myths vs. Facts

There is a lot of bad advice floating around the internet regarding home coverage. Let us clear the air and look at what is actually true.

Here is a quick breakdown of common myths versus reality:

Common Homeowner Myth: The Actual Fact

Myth: My policy will cover any leak, no matter what caused it. Fact: Policies only cover sudden, accidental damage. If your leak is from 15 years of gradual wear, it is on you to pay for it.

Myth: If my old roof gets damaged, I get a brand-new one for free. Fact: If your materials are over 10 to 15 years old, heavy depreciation applies. You will only receive a fraction of the cost for a new one.

Myth: My rates will double the second I file a claim. Fact: While rates can go up, a single claim for an unavoidable act of nature (like a regional hailstorm) rarely causes massive individual rate spikes.

Factors That Affect Your Approval

Several hidden factors determine whether your roof damage insurance payout gets approved or denied.

- The Age of the Structure: If your home is over 20 years old and you have never updated the exterior, companies are highly likely to deny claims, citing negligence.

- The Materials Used: Asphalt shingles wear out much faster than heavy metal or terracotta tiles. Your payout calculations heavily depend on the durability of what was originally installed.

- Your Personal Claim History: If you file a claim every single year for minor things, you are labeled a high-risk client, making future approvals much harder.

Tips to Maximize Your Payout

Want to ensure the company says “yes”? Keep meticulous maintenance records. If you have receipts proving you hire a professional to clean your gutters and inspect your shingles every year, the company cannot claim you neglected your property. Furthermore, if you upgrade to impact-resistant materials during your repairs, please let your agent know! You can save on your future premiums.

Average Costs, Timelines, and Payouts for Roof Claims

You may wonder how much money is at stake. While every house is different, we can look at industry averages to give you a solid baseline.

Based on recent 2026 reports surrounding home repair data across the US and urban areas like Pakistan, here is what you can generally expect when dealing with severe weather.

Type of Sudden Damage Average Claim Payout Average Timeline to Close

Severe Hail Damage $10,000 – $20,000 USD 4 to 6 weeks

High Wind Damage $8,000 – $15,000 USD 3 to 5 weeks

Fallen Tree Impact $15,000 – $30,000+ USD 6 to 8 weeks (complex structural repair)

The Impact of Your Deductible

Do not forget about your deductible! In recent years, many companies have shifted from flat-rate deductibles (such as $1,000) to percentage-based deductibles for wind and hail losses.

This means your deductible might be 1% or 2% of your home’s total insured value. If your home is insured for $300,000, a 2% deductible means you must pay $6,000 out of your own pocket before the insurance check covers the rest. Double-check this number before filing a claim for minor damage, as the repair cost is lower than your deductible!

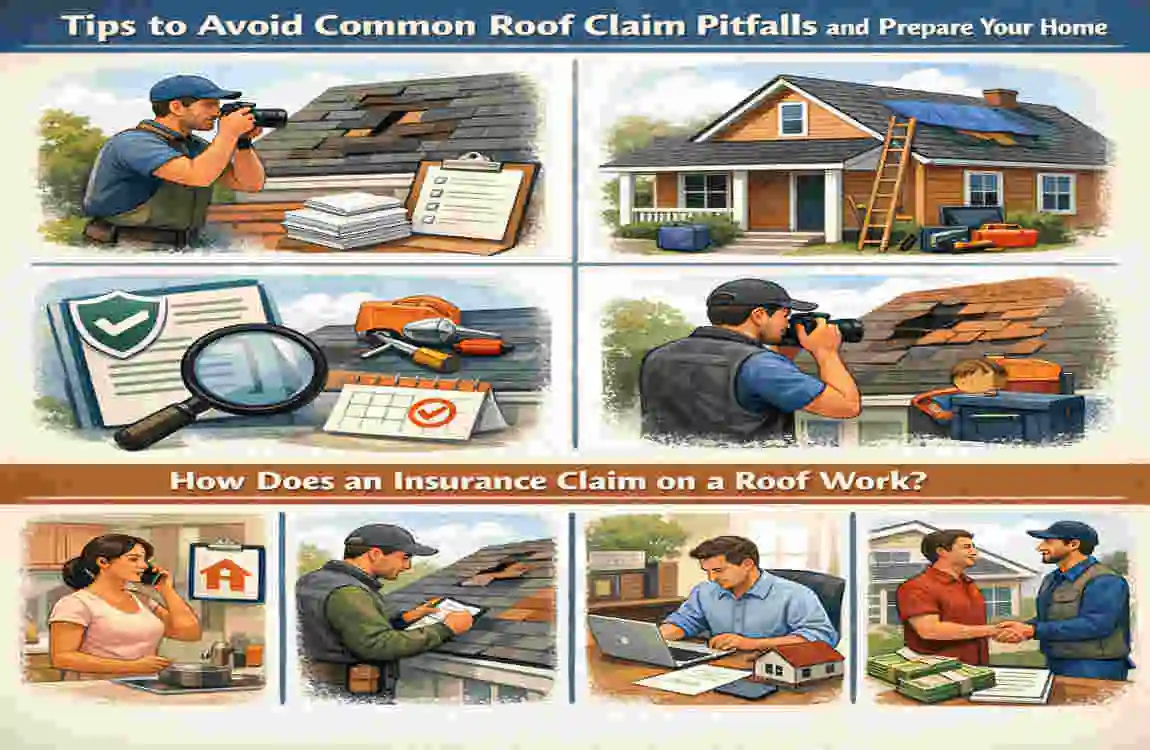

Tips to Avoid Common Roof Claim Pitfalls and Prepare Your Home

The best way to win an insurance battle is to prepare for it before the storm ever hits. Here are a few actionable steps you can take today to protect your biggest asset.

Your Preventive Maintenance Checklist:

- Get an Annual Inspection: Pay a local pro a small fee to check your property every spring.

- Clean Your Gutters: Blocked gutters force water under your shingles, causing rot that insurance won’t cover.

- Trim Your Trees: Keep heavy branches cut at least 10 feet away from your house to prevent impact damage.

Boost Your Approval Odds: When a storm is approaching, take a quick timestamped video of your property. If damage occurs, you now have undeniable proof of exactly what the structure looked like 24 hours prior. Furthermore, never settle for just one estimate. Always gather multiple bids from contractors to prove to the adjuster that your repair costs are accurate for the current market.

Should You Hire a Public Adjuster? If your claim is massive, complex, or being unfairly denied, you may hire a Public Adjuster. Unlike the company’s adjuster, a public adjuster works directly for you. They handle the negotiations and fight for a higher payout. The con? They usually take a 10% fee from your final check.

Frequently Asked Questions (FAQs)

How long does a roof claim take from start to finish? On average, a standard weather-related claim takes about 30 to 60 days to resolve. This includes the initial filing, the adjuster’s inspection, the approval process, and the delivery of the final payout check.

Will my insurance company drop me if I file a roof claim? It is highly unlikely that a single claim for an unavoidable act of nature (like a hailstorm) will cause your provider to drop you. However, if you file multiple claims in a short period, they may choose not to renew your policy.

Do I have to use the contractor the insurance company recommends? No! You have the legal right to choose any licensed, reputable contractor you want. We highly recommend gathering your own quotes from trusted local experts rather than unthinkingly using the company’s preferred vendor.

What happens if the adjuster’s estimate is too low? Do not accept a lowball offer. Ask your personal contractor to review the adjuster’s estimate, identify any missing items or hidden damage, and submit a revised quote (a supplemental claim) directly to the insurer for further negotiation.

Can I keep the claim money and fix the roof myself? If you have an Actual Cash Value policy, you can technically keep the initial check, but doing the work yourself is incredibly risky. If you have a Replacement Cost Value policy, you must provide invoices proving that a professional completed the work to get the second half of your payout.